boAt crossed ₹3,000 crore in revenue without a single breakthrough technology.

No proprietary chip. No patented acoustic design. No manufacturing facility. The earphones are sourced from ODM factories in Shenzhen. The smartwatch hardware is largely commoditised. The cables that started the company were — and remain — commodity products that any supplier can replicate in 90 days.

What boAt built was not a product company. It built a growth engine. And understanding that engine is more valuable for most Indian founders than anything in the standard D2C playbook.

This is a full teardown: how the engine was built, the real numbers behind ₹3,117 crore in FY23 revenue, where the cracks are showing, and what is directly applicable to founders building in India today.

Company snapshot

| |

|---|

| Founded | 2016 |

| Founders | Aman Gupta, Sameer Mehta |

| Category | Consumer electronics — audio & wearables |

| FY23 Revenue | ₹3,117 crore |

| FY23 Net Loss | ₹129 crore |

| India Market Share | ~27% (wearables, #1 brand) |

| Funding raised | ~$177M (Sequoia, Warburg Pincus, Innoven) |

| Peak valuation | ~$1.4 billion |

| IPO status | Filed Jan 2022, withdrawn; refile planned |

| Customers | 80M+ (claimed, lifetime) |

| Manufacturing | ~80% China/Taiwan ODM |

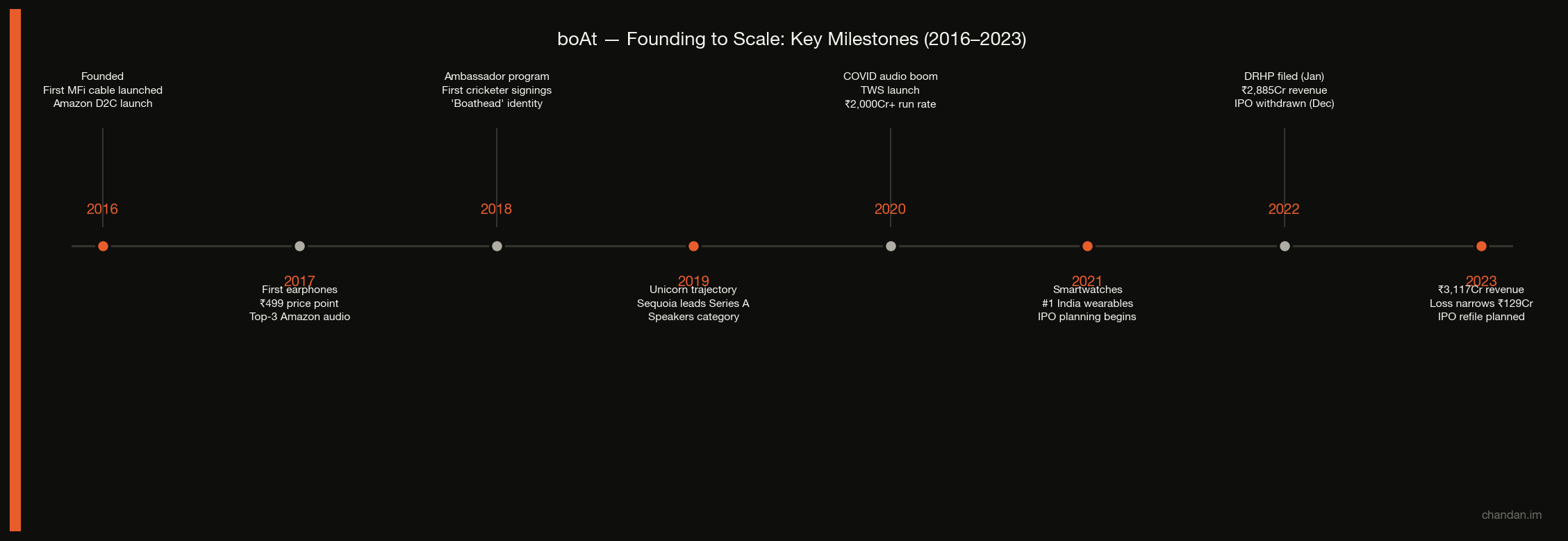

Founding to scale: the milestones

The origin story is deceptively simple. Aman Gupta’s wife was frustrated with cheap iPhone cables breaking. Aman had spent time at JBL India (Harman International) in business development. He understood exactly how the premium audio market was structured in India: Sony and JBL owned the ₹3,000+ segment, Chinese no-brands owned the ₹200–₹500 segment, and the ₹500–₹1,500 “affordable premium” segment was a white space that nobody with a real brand identity was serving.

The first product was an MFi-certified Apple lightning cable — certified, durable, and priced at ₹599. Not cheap. Not expensive. Exactly where the gap was.

The founding insight most people take from this story: find a problem in your own life. The real founding insight: the product almost doesn’t matter if you correctly identify the price-to-trust gap in your category. The cable was a vehicle for entering the segment. The plan was always to build the brand that would own the segment.

The market they were entering

The Indian wearables market in 2016 was in early formation — dominated by imports, characterised by poor quality at low price points and genuine premium pricing at the top. The structural tailwinds that made boAt’s timing exceptional:

Jio’s 2016 disruption. The Reliance Jio launch in September 2016 added 300+ million new smartphone users within three years. Most of them were first-time internet users in Tier 2 and Tier 3 cities. First-time smartphone owners need earphones. boAt entered the market exactly as this demand wave was forming.

Amazon and Flipkart reach. By 2016, Indian e-commerce infrastructure was already scaled enough to give a bootstrapped brand national distribution. boAt did not have to build logistics — they inherited it.

The Bluetooth audio inflection. TWS earphones were a nascent category in 2016 but clearly on a steep adoption curve. boAt could see where the category was going before most competitors committed manufacturing capacity to it.

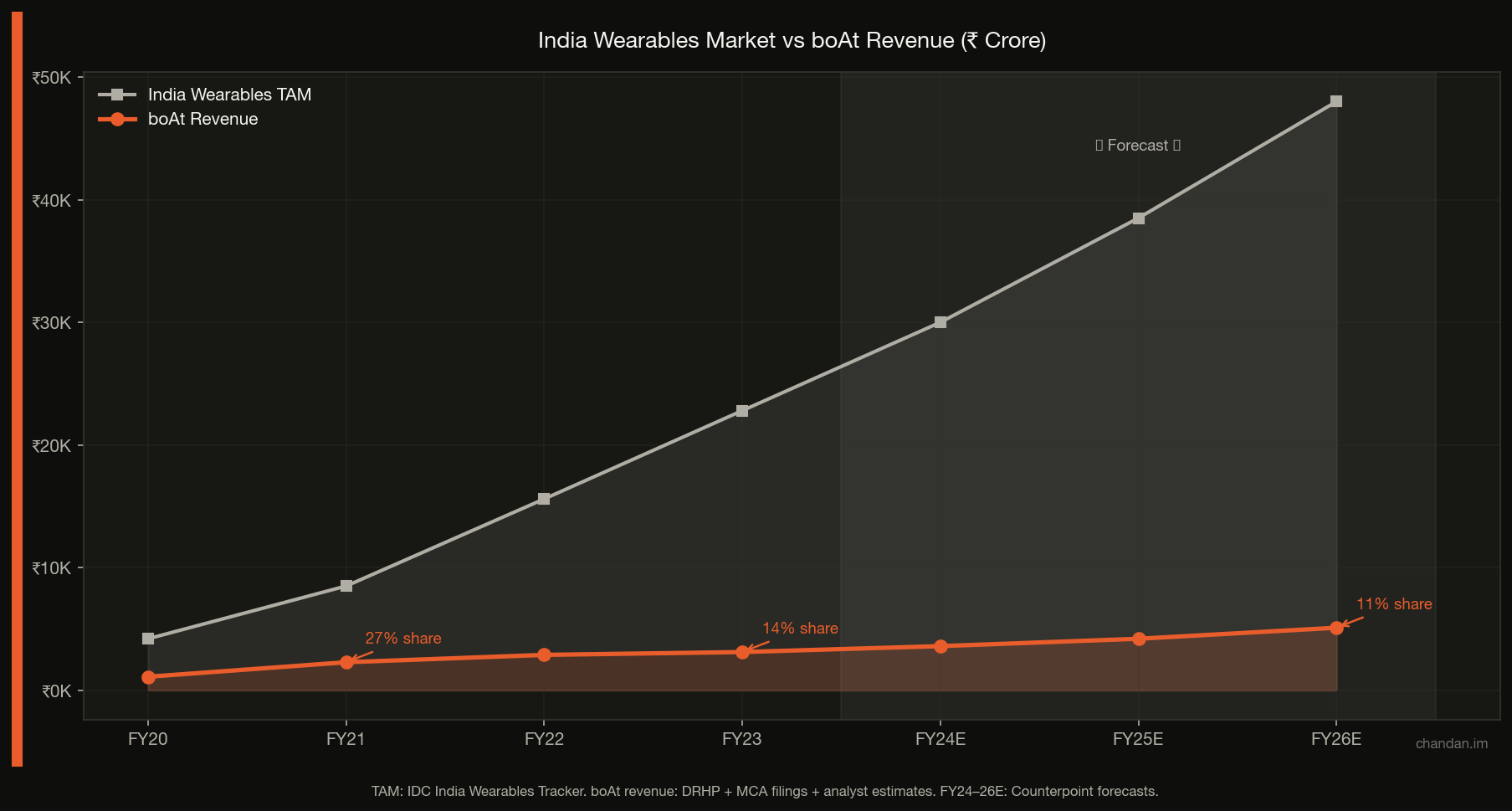

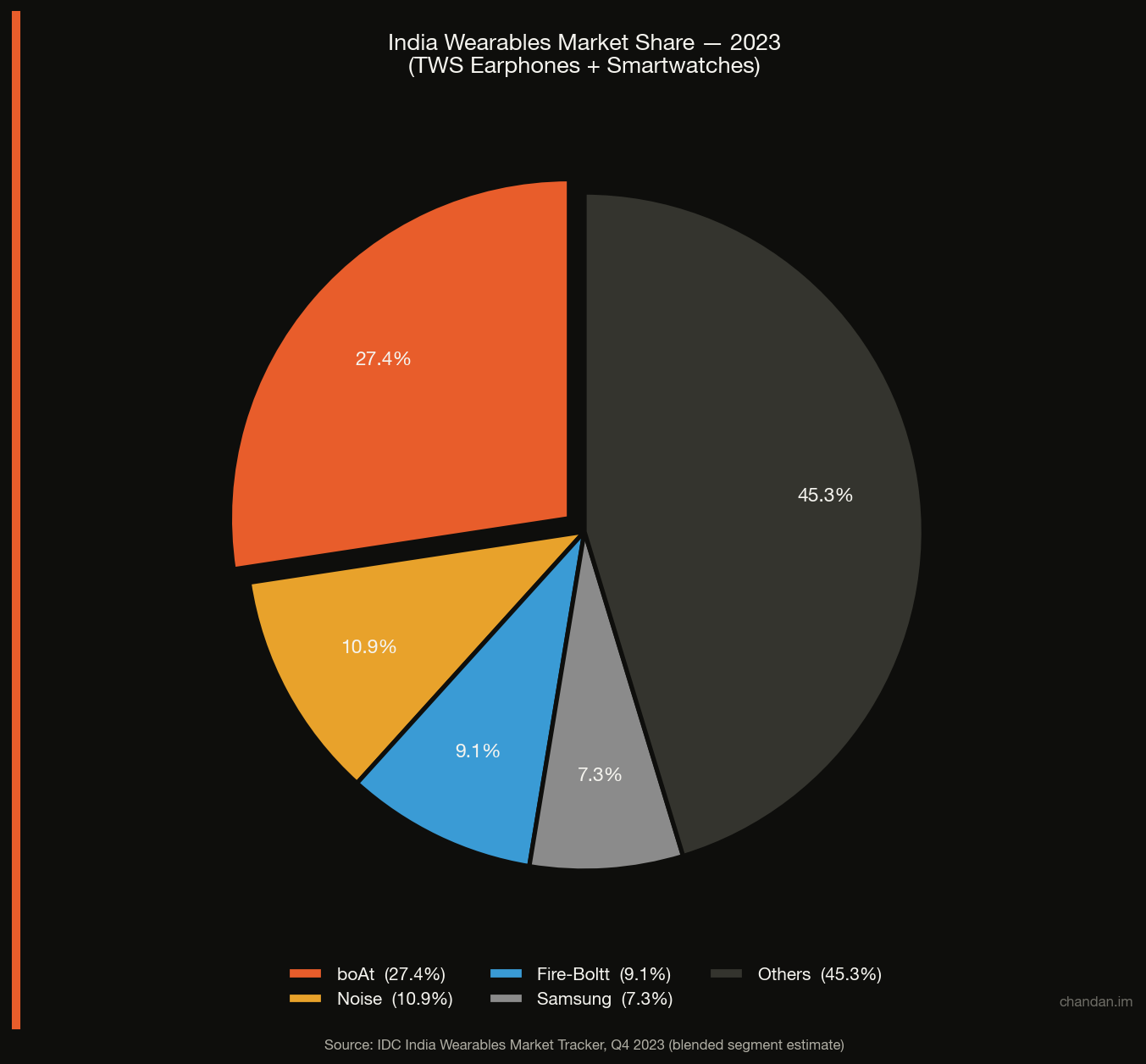

By FY23, the India wearables market had grown to approximately ₹22,800 crore with a compound annual growth rate of ~35% over five years. boAt captured ~14% of that market by revenue — a significant share in a market they helped create.

How they acquired the first 1 million customers

The Amazon-first strategy

Most D2C case studies celebrate building your own website, your own logistics stack, your own customer relationship. boAt did the opposite. They built on Amazon first — not as a secondary channel, but as primary distribution infrastructure.

This was a deliberate strategic choice with three concrete effects:

Zero logistics cost at launch. Amazon Fulfilled by Amazon (FBA) meant no warehouse investment, no last-mile headache, no cash locked in inventory infrastructure. boAt was asset-light at precisely the stage when capital efficiency mattered most.

Built-in discovery engine. Ranking in “earphones under ₹1000” on Amazon delivered reach that would have cost crores in paid acquisition. boAt engineered its products specifically for marketplace ranking: pricing calibrated to hit the key filter thresholds, review velocity built aggressively in early months, product imagery optimised for conversion at thumbnail size.

Credibility transfer. In 2016–2018, a meaningful fraction of Indian consumers trusted Amazon-listed products over brand-direct websites they had never heard of. The “Fulfilled by Amazon” tag served as a trust signal that boAt’s own site could not have generated in year one.

The structural cost: an estimated 60–70% of boAt’s revenue still runs through Amazon and Flipkart. The marketplaces have significant pricing and promotional power over boAt’s margins. The move to genuine D2C — own-site revenue, first-party customer data, direct relationships — remains slower than the company wants.

But at launch, it was the correct call. Reach without capital destruction is the right priority for a bootstrapped brand in a commoditised hardware category.

The ambassador timing play

The boAt ambassador story is usually told as: they signed 80 celebrities and became ubiquitous. The actual play was more surgical than that.

The key variable was timing. boAt signed ambassadors at the inflection point — just before or just as the celebrity was breaking out nationally. KL Rahul when he was emerging, not established. Disha Patani after MS Dhoni: The Untold Story but before she commanded top-tier commercial rates. Kiara Advani after Kabir Singh’s box office success but before she hit A-list pricing.

The economics of timing advantage are significant. An ambassador signed at emerging-star rates and carried through their national breakout provides the perception of having spent at peak-fame rates — at a fraction of the actual cost. Competitors watching from the outside see boAt everywhere with major celebrities and assume a massive marketing budget. The actual cost-per-impression is far lower than it appears.

The second dimension: breadth over depth. 80+ ambassadors across cricket, Bollywood, OTT, kabaddi, football, and esports means boAt shows up in every youth culture vertical simultaneously. No single competitor can afford this coverage because they are building concentrated premium positioning in narrower segments. boAt’s strategy trades depth for omnipresence — making the brand feel culturally inevitable to a wide audience rather than aspirational to a narrow one.

This is the ambassador equivalent of long-tail SEO. Most brands fight for the expensive head terms (top 5 celebrities). boAt dominated the mid-tier long tail and won brand recall at lower total cost.

The most underanalysed element of boAt’s early growth was the construction of a tribal identity.

boAt made their customers a club. Not a loyalty programme with points. An identity. If you used boAt products, you were a Boathead — part of a tribe of people who valued music, sport, and self-expression at a price point that was honest about where they were in life.

The mechanics were not complex: community social media pages, user-generated content campaigns, product names drawn from music culture, limited drops tied to cultural moments. But the effect was powerful: retention became identity-driven rather than product-driven.

This matters for the growth equation because most consumer electronics brands treat repurchase as a product problem — the customer replaces the product when it breaks. boAt created a category where repurchase was a community behaviour. Boatheads upgraded when new products dropped, not just when old ones failed. They tried different form factors — earphones and headphones and speakers and smartwatches — because the brand had earned permission across the entire audio and wearables category.

The revenue model: what the numbers actually say

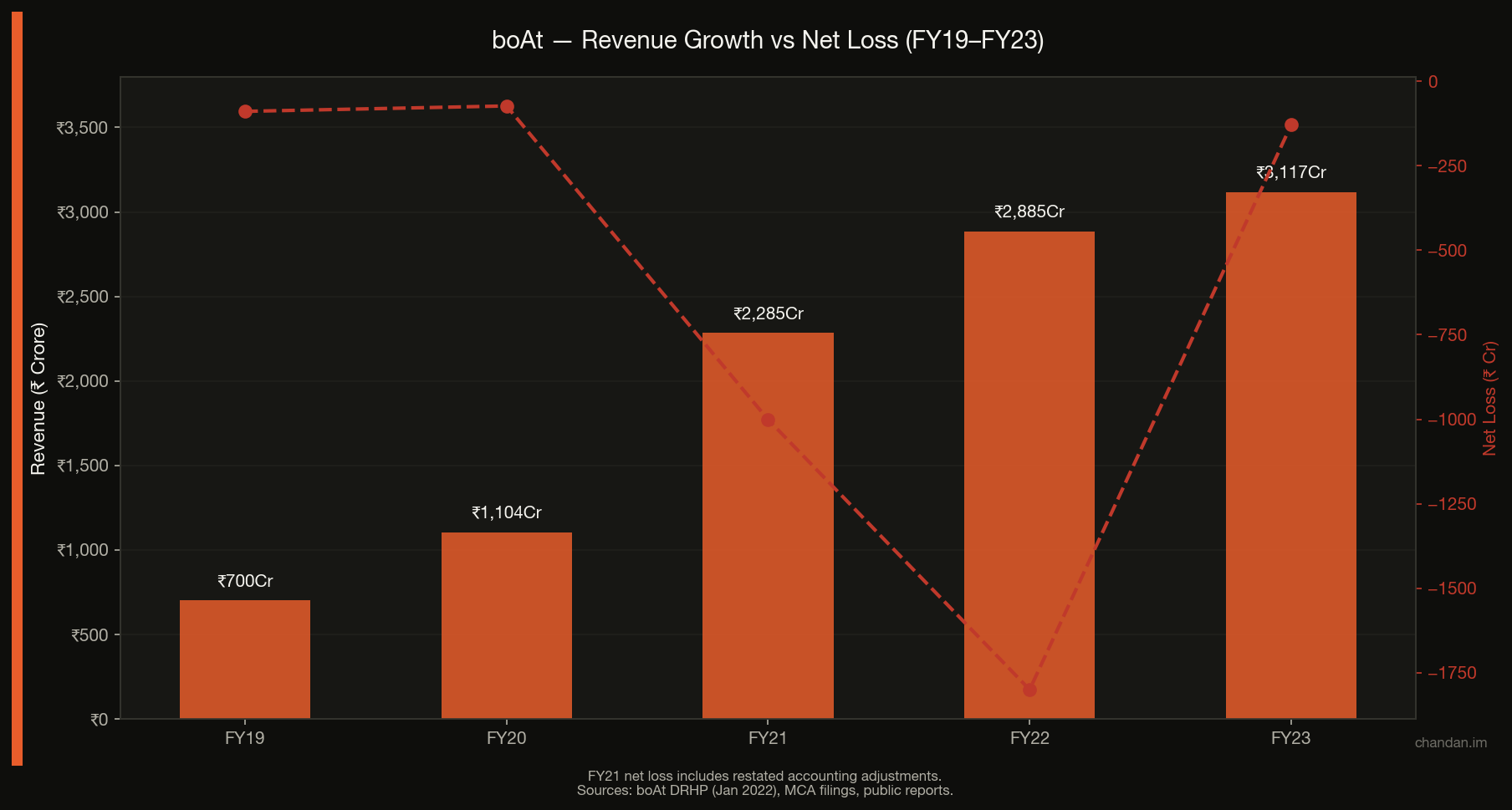

FY23 Revenue: ₹3,117 crore

FY22 Revenue: ₹2,885 crore

YoY Growth: 8.1%

Net Loss FY23: ₹129 crore

The 8% growth rate from FY22 to FY23 is the most important number in this dataset — and the most underreported. boAt grew at 100%+ in FY21 and 26% in FY22 as pandemic-driven audio demand surged. The deceleration to 8% in FY23 signals that the tailwind is gone and boAt is in a genuine competitive market where growth must be earned, not inherited from category expansion.

Revenue breakdown

Wired audio (earphones + cables): The products that launched the company remain meaningful contributors. Wired earphones are now lower-margin than wireless but require less consumer education and have high replacement frequency — every broken earphone is a repeat purchase opportunity.

True wireless stereo (TWS) earphones: The category boAt moved into in 2020 and that now anchors the portfolio. Higher average selling price (₹1,500–₹3,000 range) versus wired, but significantly more competitive from established players (Samsung, OnePlus, Nothing) moving down-market.

Smartwatches: Entered in 2021 and rapidly became a significant revenue contributor. The category is growing faster than audio in India, but Fire-Boltt and Noise have established strong positions, and the competitive pressure on ASP is intense.

Speakers and accessories: High-margin relative to earphones, but smaller addressable market. Mostly supplementary to the core audio business.

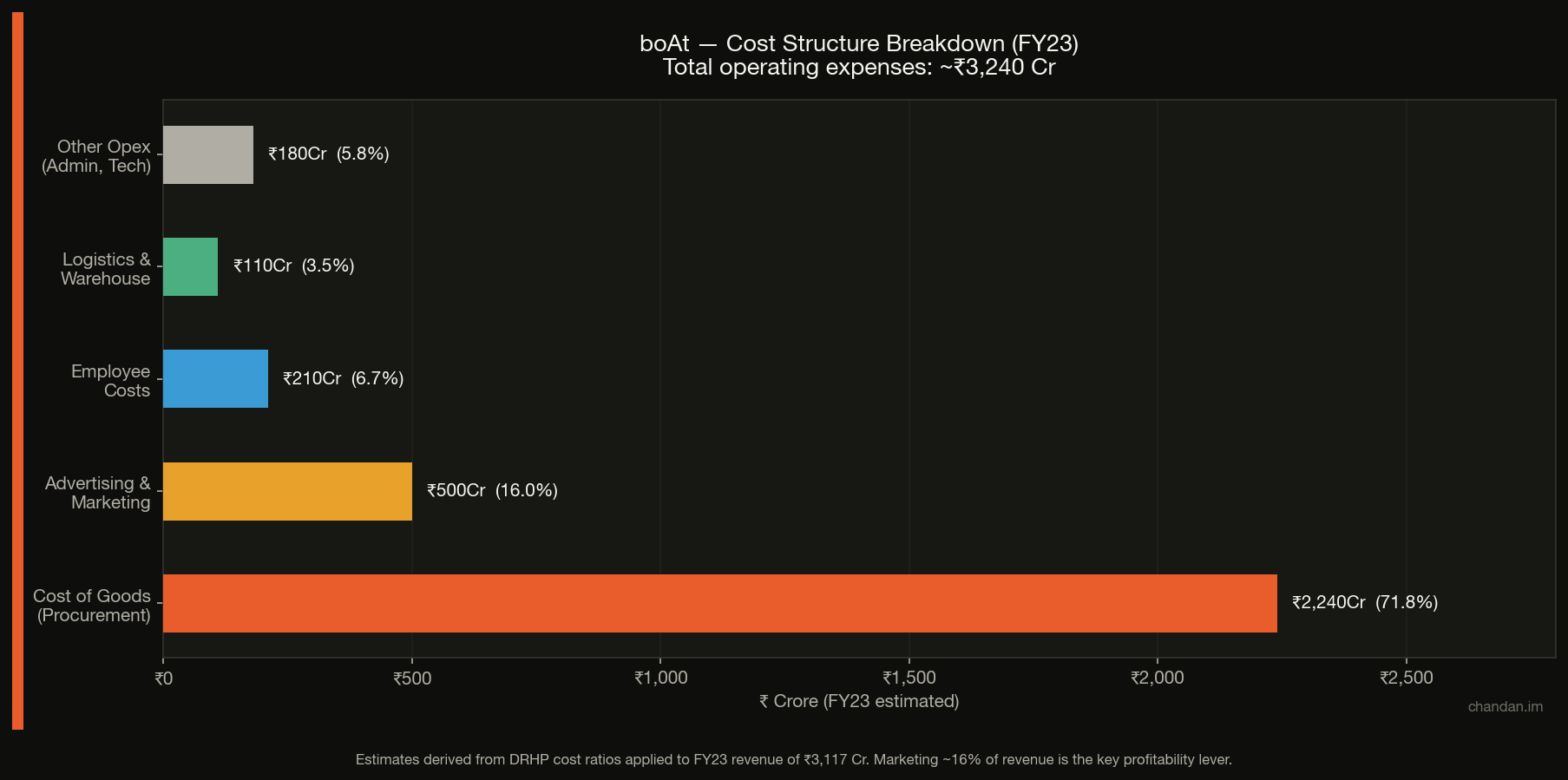

The cost structure

The cost structure reveals the central tension in boAt’s business: the brand investment required to maintain market leadership consumes most of the gross margin that the hardware generates.

Cost of goods — ~₹2,240 crore (~72% of total costs): This is the procurement cost of hardware from Chinese and Taiwanese ODM manufacturers. The margin structure here is industry-standard for ODM-dependent electronics brands: gross margins of 25–30% before marketing and operating costs. The PLI (Production Linked Incentive) scheme for electronics is creating some incentive to shift manufacturing to India, but Indian unit economics are currently 20–30% higher per unit than Chinese manufacturing.

Advertising and marketing — ~₹500 crore (~16% of revenue): This is the ambassador program, IPL and cricket sponsorships, digital performance marketing, and offline activations. This is not waste — it is the structural cost of maintaining the brand position in a commoditised hardware category. Without it, there is nothing preventing a consumer from buying the identical hardware spec from a cheaper, unknown brand.

Employee costs — ~₹210 crore: Have grown significantly as the company has built engineering, product, and corporate functions ahead of the planned IPO refiling.

Logistics and warehousing — ~₹110 crore: Surprisingly lean given revenue scale, a direct benefit of the marketplace-first distribution strategy.

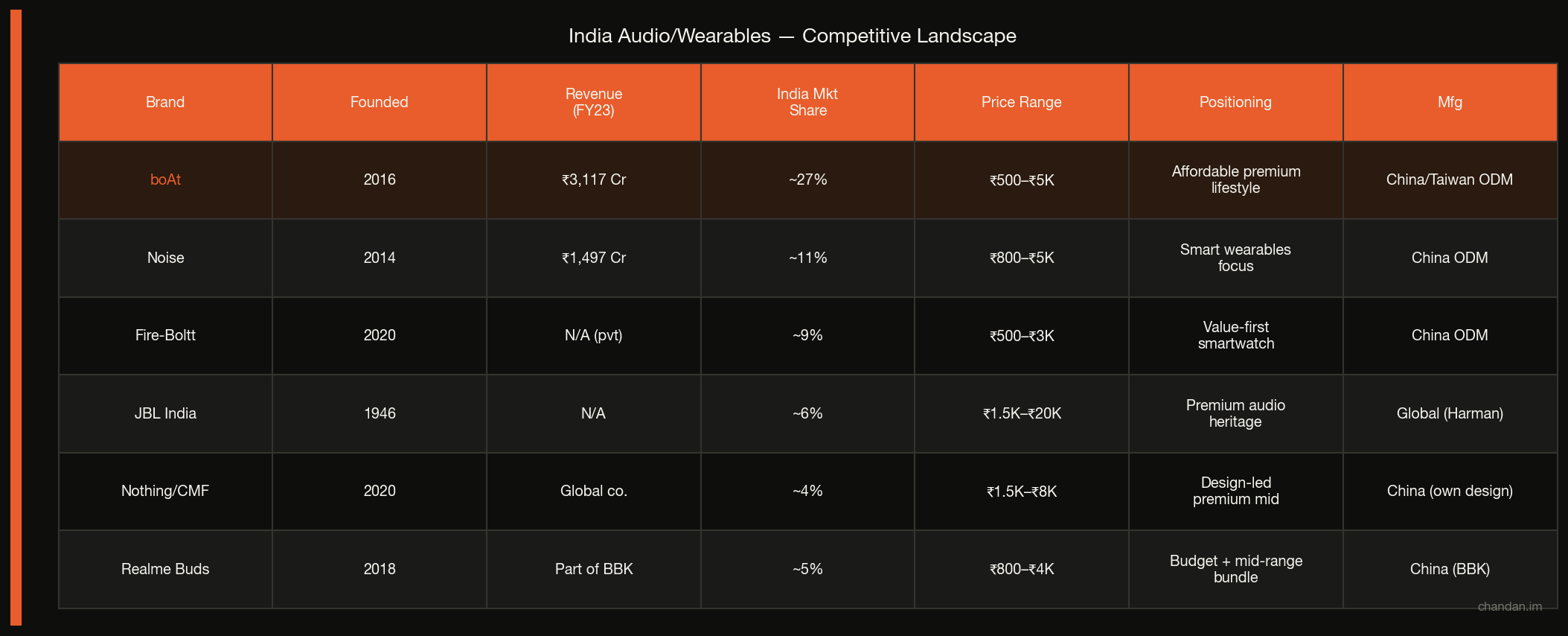

The competitive landscape

The market boAt created in 2016–2018 is now a genuinely competitive space. Five dynamics define the current landscape:

Noise (11% share): The most direct competitor. Similar founding DNA (India-first, affordable premium, D2C marketplace), but with a stronger smartwatch positioning than earphones. Noise filed for IPO in 2023 and withdrew similarly to boAt. The two companies are running almost identical playbooks with the same profitability challenge.

Fire-Boltt (9% share): Youngest of the major players (2020) but grew explosively in smartwatches by undercutting on price. Revenue and profitability data is not public. The strategy appears to be volume-over-margin in smartwatches, which creates pressure on boAt’s ASP without necessarily threatening brand perception.

JBL India (6% share in accessible segments): Harman/JBL moved aggressively down-market in 2022–2023, launching products in the ₹1,500–₹3,000 range that compete directly with boAt’s mid-tier. The JBL brand carries international audio credibility that boAt cannot match in direct comparison — the competitive risk is real for the aspirational consumer who now can afford a “real” audio brand at boAt-comparable prices.

Nothing / CMF (4% share and growing): The most strategically interesting entrant. Carl Pei’s CMF brand specifically targets the ₹1,500–₹5,000 premium-accessible segment with stronger design aesthetics and a technology narrative (transparent design, software integration) that boAt cannot easily replicate. CMF is winning consumers who want to feel like they are buying something designed, not just branded.

Samsung Galaxy Buds ecosystem: For consumers with Samsung smartphones, the Galaxy Buds entry-level SKUs at ₹2,000–₹3,000 represent a trust-based competitive threat. Samsung’s India retail footprint and device integration are advantages boAt cannot match.

The market share chart tells the real story: boAt’s 27% share is dominant, but the “Others” category (45%) is where the next wave of share loss is most likely to come from — fragmented competitors finding niches that boAt’s broad-based strategy does not serve deeply enough.

The growth moat: honest assessment

boAt’s defenders argue the brand is the moat: the Boathead identity, the ambassador network, the cultural ubiquity are expensive and slow to replicate.

This is partially true. Brand takes years and consistent investment to build. A new entrant cannot outspend boAt to an equivalent position in 12 months.

But the moat is weaker than it appears for three structural reasons:

The price gap has closed. In 2016, boAt had near-exclusive ownership of the ₹500–₹1,500 audio segment with genuine brand value. In 2024, Noise, Fire-Boltt, Realme, OnePlus, and Nothing are all competing in adjacent or overlapping price bands. The white space that defined boAt’s founding opportunity is now a crowded centre.

The products are replicable in 90 days. The hardware is ODM. Any sufficiently funded competitor can launch a product matching boAt’s spec sheet within a quarter. The brand must do more work as the product differentiation gap has compressed to near-zero.

The ambassador model cost structure has deteriorated. Celebrities who were emerging when boAt first signed them are now established stars commanding market rates. New generation ambassador negotiations happen in a market where 40+ D2C brands are competing for the same talent. Cost-per-impression from the ambassador program has risen steadily since the 2018–2020 golden period.

The honest assessment: boAt has a brand advantage, not a structural moat. The brand advantage is real and valuable. It requires continuous, expensive investment to maintain. That continuous investment is the primary reason the company is not yet profitable — and the primary question for its IPO readiness.

What broke — and when

The FY23 deceleration is the canary. What specifically changed:

The COVID audio tailwind reversed. The work-from-home, online learning, and streaming boom drove 100%+ growth in FY21 and significant carry-through in FY22. FY23 was the first normalised year. The underlying organic demand is good but not extraordinary.

Amazon CAC rose. boAt’s historical competitive advantage on marketplace ranking — optimised pricing, aggressive review velocity — has been eroded as every competitor learned the same playbook. Sponsored placements on Amazon are now mandatory for any brand wanting category visibility, adding a paid acquisition cost layer to what was originally organic marketplace growth.

Smartwatch competition intensified faster than expected. Fire-Boltt entered the smartwatch category and grew market share aggressively through price compression. The category boAt expected to own after audio wearables has turned into a margin-pressuring battle fought primarily on price.

The IPO withdrawal cost intangibles. Filing and then withdrawing a DRHP creates questions — about financials, about growth trajectory, about capital market confidence — that take time to resolve regardless of the underlying business health.

What Indian founders can steal

1. Use marketplace infrastructure as D2C before you build D2C.

Amazon and Flipkart gave boAt national distribution, customer trust transfer, and logistics infrastructure at zero fixed cost. The right sequence for hardware startups: earn product-market fit on marketplaces first. Build own-site D2C after you have brand equity and data. Most founders do this backwards and pay a high capital cost for D2C infrastructure before the product is validated.

2. The mid-tier ambassador play compounds.

Sign three people who are six months from national fame. The timing advantage gives you A-list perception at C-list cost. This works in food, fashion, fitness, fintech — anywhere celebrity association builds trust. The critical skill is reading which emerging talent is genuinely on a breakout trajectory versus which one has already peaked without breaking through.

3. Tribe identity beats loyalty programme every time.

“Boathead” is worth more than any points-and-rewards system. Give your customers a name, a shared identity, and content that makes that identity feel real. Retention that is anchored in identity is fundamentally harder for competitors to poach than retention anchored in price or product features.

4. Category expansion speed beats category depth in commoditised hardware.

boAt never went deep on acoustic R&D. They went wide — into every audio form factor, then into wearables — faster than any competitor could match. In categories where the hardware is commoditised and the brand does the work, breadth compounds faster than depth. Know which type of market you are in before deciding where to invest.

5. Brand investment during growth is not discretionary.

The single most expensive mistake Indian consumer brands make is treating marketing as a post-profitability luxury. boAt’s 2018–2021 brand investment during the growth phase was the engine that sustained growth through the competitive compression of 2022–2024. Brands that starve marketing to reach profitability faster usually find that by the time the market matures, they have neither the margin nor the brand equity to hold their position.

The path forward

boAt’s IPO story is not over — it is paused. The refiling path requires demonstrating net profitability or a credible trajectory toward it. The levers are clear:

- India manufacturing via PLI: Lower COGS by 15–20% on PLI-eligible products as localisation scales. Longer timeline than publicly stated, but the direction is right.

- Services attach rate: Extended warranty, repair services, and software-driven features can add 3–5% of revenue at high margins. Currently underdeveloped.

- Marketing efficiency: As brand recognition matures, the incremental return on ambassador spend should improve. The question is whether the competitive environment allows any reduction in marketing intensity.

- Category leadership in smartwatches: If boAt can stabilise smartwatch market share above 20% as the category grows to ₹10,000 Cr+, the revenue scale could support the profitability investors want to see.

The business is real. The brand is real. The challenge is translating both into the profitability story that a public market listing requires — in an environment where every competitor has studied the boAt playbook and is executing a version of it.

Chandan Kumar is a full-stack growth marketer and founder of Grovio Labs. He has spent 10+ years building growth systems for Indian brands across acquisition, retention, and monetisation. He advises a small number of companies per quarter — see how it works. Related: Growth Marketing in India: What Western Playbooks Get Wrong · The Indian D2C Retention Problem.